Introductory statement at the press conference presenting the Annual Report 2025

Check against delivery.

1 Welcome

Ladies and gentlemen,

Welcome to our annual accounts press conference.

First Deputy Governor Sabine Maunderer will explain the Bundesbank’s annual accounts to you in more detail in just a few moments.

I would like to start by saying a few words on the developments in the Middle East: the economic repercussions of the war will depend largely on how long the conflict continues. They could arise through a variety of channels. At present, the most significant of these are oil and gas prices: they have risen considerably. For monetary policy, the crucial factor is whether these are temporary supply shocks that we should look beyond.

If the conflict comes to a swift end, a political agreement is reached, and there is, at most, minimal damage to the energy infrastructure in the region, then energy prices could soon fall again. In this case, the consequences for inflation would be short-term and limited overall. By contrast, if energy prices were to remain elevated for an extended period of time, this would tend to lead to higher inflation and weaker economic activity in the euro area.

It is still too early to draw any monetary policy conclusions from this volatile situation. We are well advised to carefully analyse the impact on our medium-term inflation target.

And this already brings us to the topics that I would like to address today: How are economic activity and prices developing? What does this mean for monetary policy in the euro area? How have developments in 2025 impacted the Bundesbank’s profit and loss account?

Let me begin with the most important point: first, after a longer period of time, price stability prevails in the euro area once again. This is the most important success for the Eurosystem.

Second, we on the ECB Governing Council are determined to stabilise inflation at 2 % on a sustainable basis. With key interest rates as they are, we are currently well positioned to do so.

Third, the Bundesbank’s balance sheet is sound. While we continue to bear financial burdens, these are easing. Our annual loss has more than halved. We can perform our tasks to the fullest extent.

I will explain this in more detail now.

2 Developments in the German economy

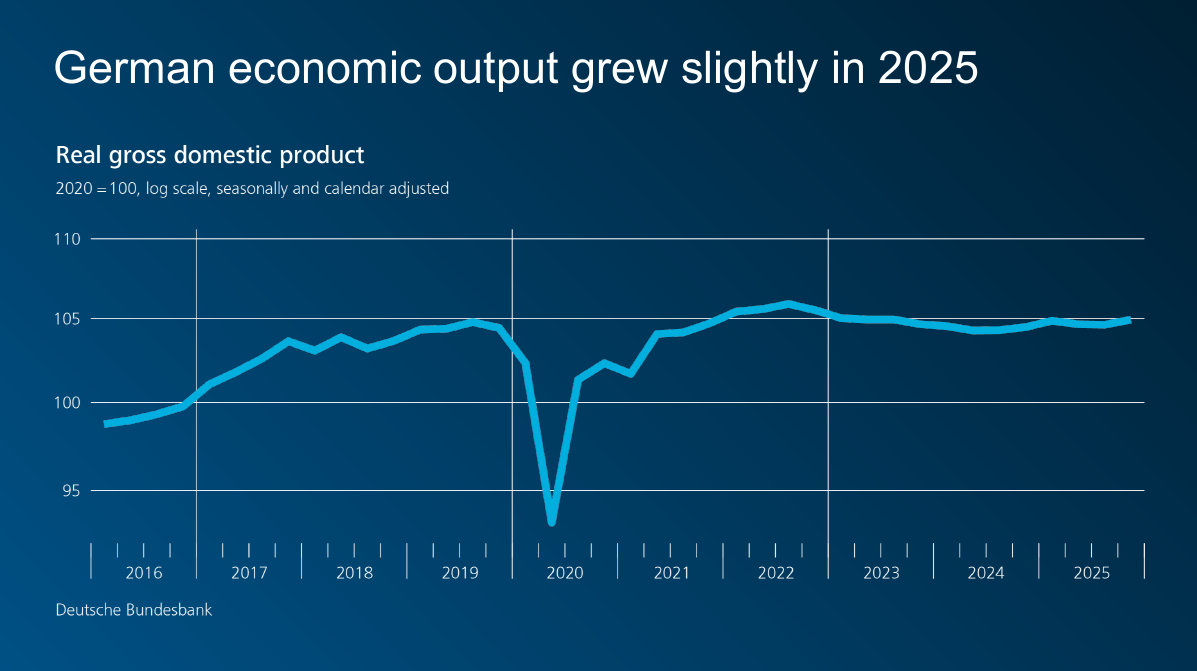

Let’s start with the German economy: when will it get past its period of weakness?

Following two years of contraction, it grew again slightly in 2025: by 0.3 % after price and calendar adjustment However, economic output is still barely higher than it was in 2019.

This growth was driven mainly by consumption. Both consumers and general government spent more here. By contrast, the weakness in investment persisted. And exports also declined once again.

German exporters have been facing headwinds for some time now. They have been losing ground internationally since 2017. According to Bundesbank analyses, this was due primarily to a deteriorated international competitive position.[1] Higher energy prices for industry are certainly a factor here, but labour costs, shortages of skilled workers, and bureaucracy also played a role. In addition, there was greater competitive pressure, especially as China has caught up with the technologically leading economies in an increasing number of areas.[2]

In 2025, additional headwinds came from the new US tariffs. It is clear that these headwinds will be a major concern for us this year, too. Consider the additional tariffs that were threatened for a time in January, the ruling of the US Supreme Court in February, the additional tariffs that were subsequently imposed for 150 days, and the uncertainty regarding whether tariffs paid will be returned and how things will proceed in the future. All of these factors are likely to encourage enterprises to focus on other markets as well.

Policymakers can provide support in building new trade relations. I welcome the fact that the European Commission wishes to implement the Mercosur agreement on a provisional basis. This is an important step on Europe’s path towards entering into new partnerships. Such impulses will help German foreign trade to regain momentum despite the harsh trade policy climate.

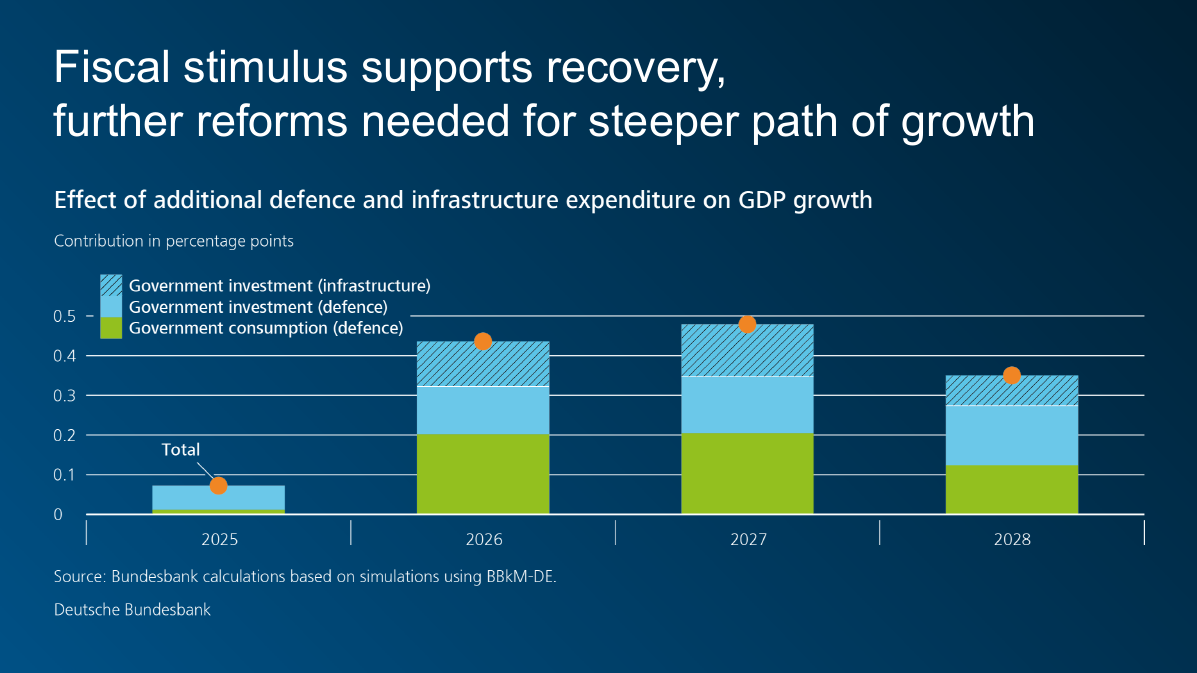

The domestic economy is likely to slowly recover again in 2026. Additional spending on defence and infrastructure is causing a substantial rise in demand from the public sector. Household demand, too, is likely to pick up slowly. Strong growth in wages is creating scope for this. As a result, economic growth will increase markedly from the second quarter onwards.

As things currently stand, it could be slightly higher for the year as a whole than was expected in our Forecast for Germany from December. This is due, above all, to a higher starting level. This is because the economy saw surprisingly strong growth in the final quarter of 2025.

Expansionary fiscal policy is giving a considerable boost to economic activity. We estimate the overall effect of additional defence and infrastructure spending until 2028 to be 1.3 percentage point of economic growth.[3] In order for these impulses to lead to a steeper path of growth over the longer term, too, we need additional, accompanying structural reforms.

Some measures have already been taken in this regard. Consider, for example, the initiatives to reduce bureaucracy and to speed up administrative processes. Now it is a question of implementing this modernisation agenda. And it should spur us on to remove obstacles to growth in other areas, too.

The Federal Government has set out a number of measures for this year, such as reforms to the social security funds. These are the “hard boards” that Max Weber once described as he explained the meaning of politics: “A strong, slow drilling” through such boards.[4] At its core, this is a two-fold appeal: it requires action on the part of policymakers, but also patience on the part of the general public.

Despite all of the challenges, we should not forget Germany’s strengths: stable institutions with reliable rules, excellent research, adaptable enterprises and highly skilled and dedicated people. If policymakers loosen the brakes on growth, and society and the economy follow suit, this could create new momentum.

3 Inflation and monetary policy in the euro area

In other places, we are better off without momentum: I am talking, of course, about inflation.

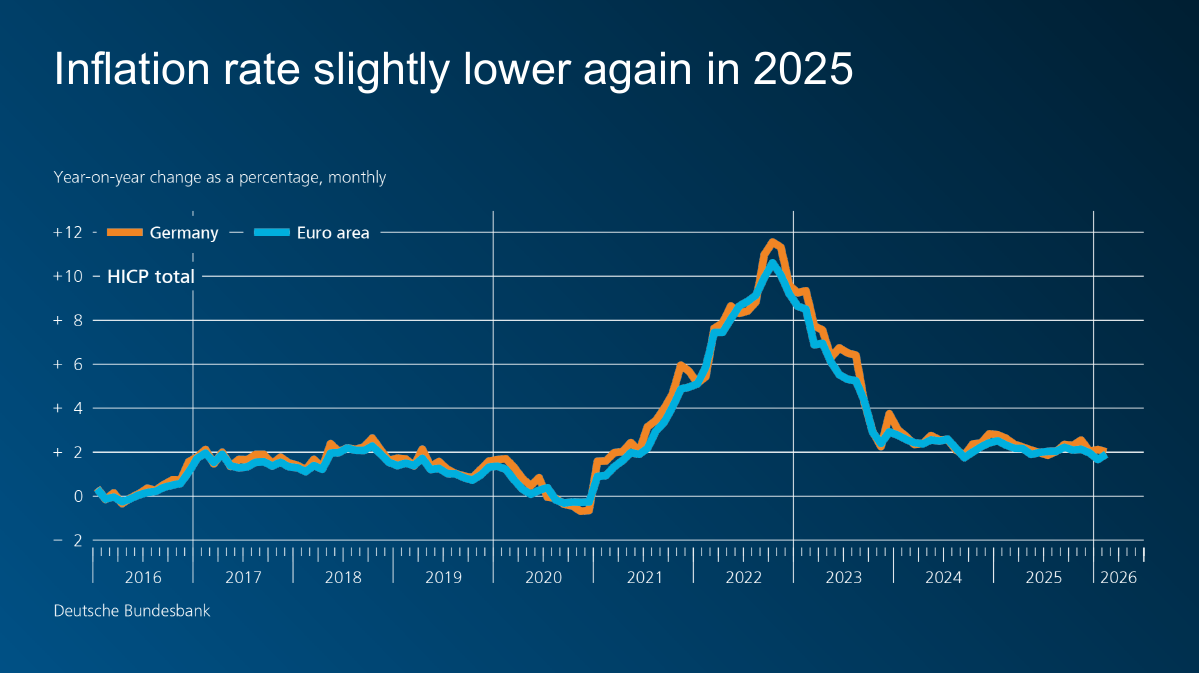

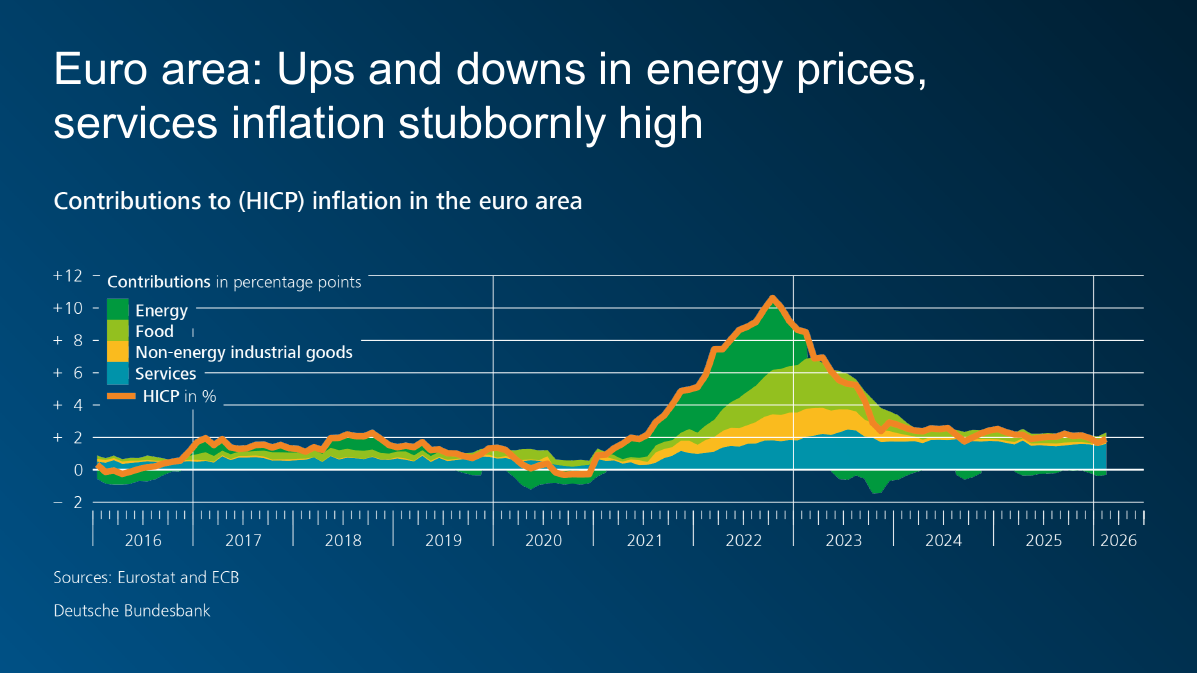

After many years in which inflation was far too high at times, we are now where we aim to be – at around 2 %. This is true for both Germany and the euro area.

This success is due, amongst other things, to the decisive action taken by the ECB Governing Council. Between July 2022 and September 2023, we raised key interest rates ten times – they peaked at 4 %. Between June 2024 and June 2025, we lowered them again. Since then, the deposit facility rate has stood at 2 %. The interest rate reversal did not trigger a recession. And financial markets also coped well with it.

The fact that national central banks of the Eurosystem and the ECB were able to take such decisive action was due to their independence. At the Bundesbank, we know from our many years of experience that central bank independence is in the very DNA of successful, effective monetary policy. This allows us to focus on our mandate and ensure price stability.

Let us take a closer look at inflation in 2025.

In Germany, it fell slightly. As measured by the Harmonised Index of Consumer Prices (HICP), it stood at 2.3 % on an annual average.

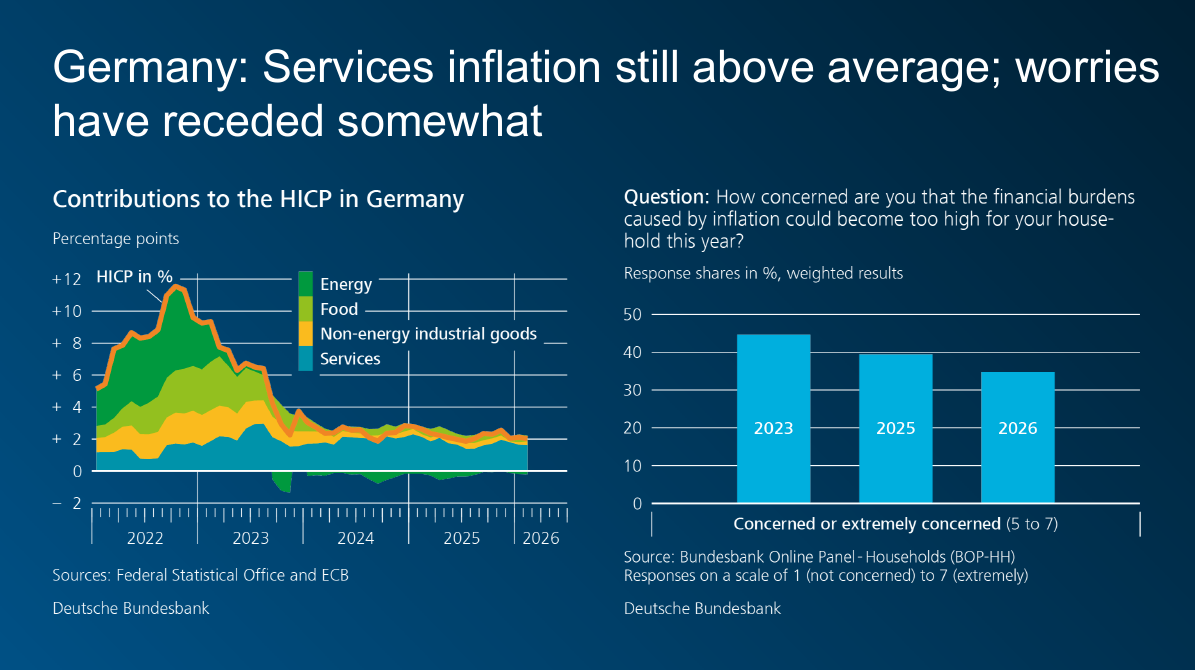

Upward pressure on food prices subsided. Energy became cheaper again, by 2.3 %. Core inflation, excluding energy and food, also declined from 3.2 % to 2.8 %. Services inflation remained higher than average, despite shrinking from 4.3 % to 3.9 %. Strong wage growth is a key factor here.

On average, higher wages have now offset the loss of purchasing power in recent years. However, surveys show that people do not necessarily feel like this is the case. Many feel poorer today than before the wave of inflation. For example, when they go shopping for groceries: on average, food costs over one-third more than in 2020. And that has quite an impact: it is food prices, in particular, that people pay attention to when gauging inflation.[5]

In addition, many people are worried about new price surges. People who go to the petrol station or fill up their heating oil tanks these days experience a price surge. However, this topic was close to people’s hearts even before this. Our household survey in January 2026 shows that more than one-third of respondents are concerned or extremely concerned about being financially overburdened by inflation this year.

The ECB Governing Council is determined to stabilise inflation at its 2 % target on a sustainable basis. This is the key monetary policy task in 2026.

From today’s perspective, we are well positioned at the current key interest rate level. If the inflation picture changes substantially, we are well placed to respond. As I have already mentioned, it is still too early to draw monetary policy conclusions from the volatile situation in the Middle East.

For the euro area, we are aiming for an inflation rate of 2 % over the medium term. The inflation outlook is therefore crucial. What is particularly interesting here is where inflation is headed beyond the short-term fluctuations.

We refer to this as underlying inflation. Metaphorically speaking, headline inflation depicts the movement of the waves on the surface of the water, including the spray caused by individual gusts of wind. Underlying inflation is more like the current below. It shows the direction in which inflation is heading.

Services inflation is important for the current. In 2025, it was consistently above 3 % and is still proving stubborn. Energy prices are currently a major factor stirring up the spray. The conflict in Iran is pushing up consumer prices through higher energy prices.

For monetary policy, it is crucial whether this results in persistent inflationary pressures or just temporary price fluctuations. We have seen how the outbreak of the war in Ukraine led to marked second-round effects through a rise in energy prices. And so we are very vigilant here.

Uncertainty has increased significantly as a result. At the ECB Governing Council meeting the week after next, we will discuss the latest data and projections. On this basis, we will then decide whether the current monetary policy stance remains appropriate or whether action needs to be taken.

4 The Bundesbank’s annual accounts for 2025

Ladies and gentlemen,

Monetary policy is reflected in a central bank’s balance sheet. This image is not a snapshot of the monetary policy decisions made in the reporting year, but rather a photograph taken with a long exposure time.

For us, this means that monetary policy measures taken over the past decade help shape today’s balance sheet. We still have large holdings of securities remunerated at low, fixed rates. These were acquired under the monetary policy asset purchase programmes. Perhaps you remember the abbreviations APP and PEPP.

Although maturing bonds are no longer reinvested, the long maturities mean that the holdings are declining only gradually. At the same time, this means that commercial banks’ deposits, which increased as a result of the asset purchases, are also declining only slowly. The interest on these deposits is paid on a short-term basis – at the current deposit facility rate, which the ECB Governing Council uses to steer monetary policy.

Since the interest rate reversal in 2022, interest expenditure on deposits has exceeded interest income from the bond portfolios. Net interest income is negative. On balance, this has led to considerable financial burdens for the Bundesbank.

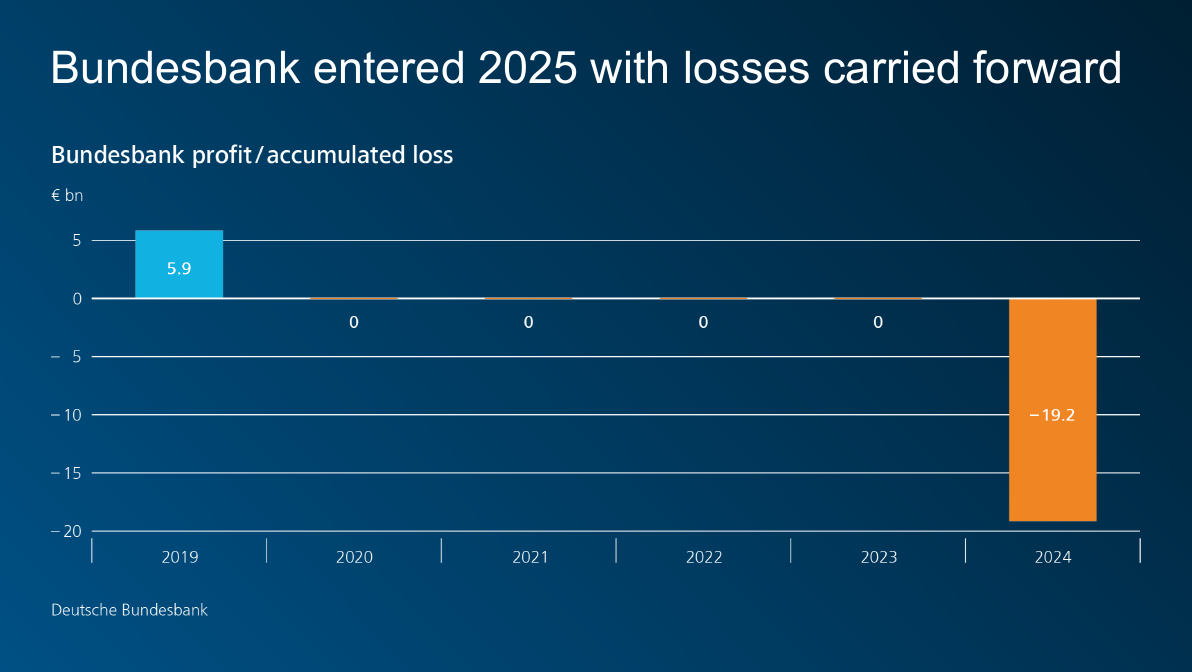

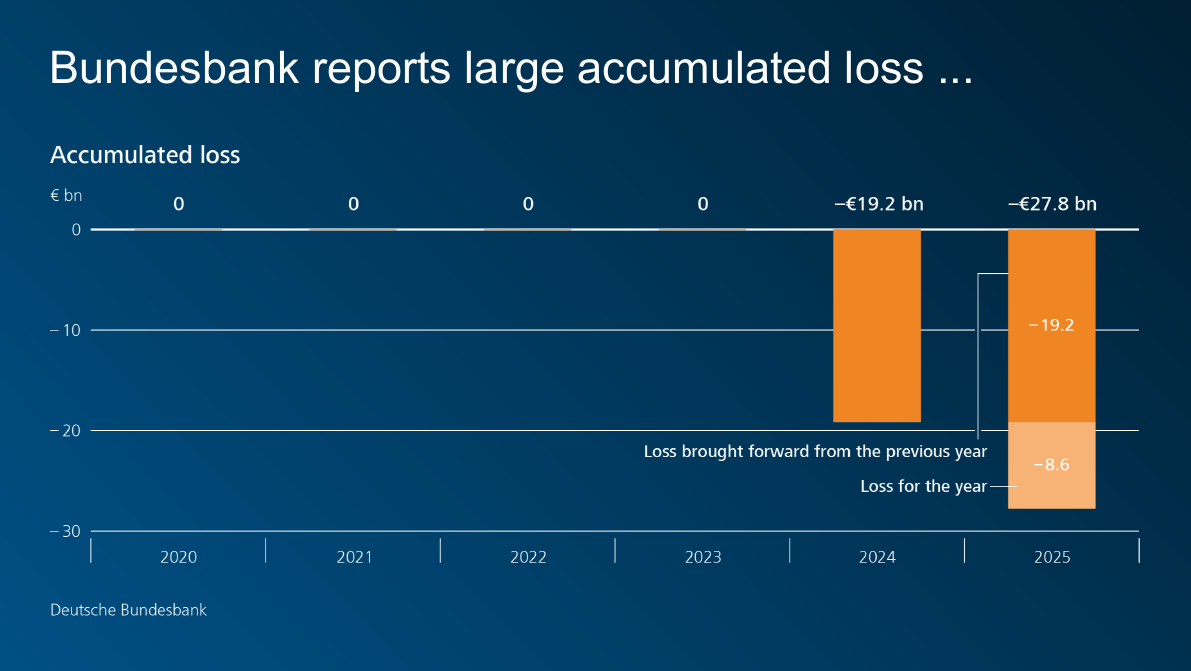

In 2022 and 2023, it was still possible to offset the losses for the year by releasing the provisions for general risk and making withdrawals from the reserves. Distributable profit came to zero. After that, however, these buffers were almost exhausted. As a result, the loss for the financial year 2024 was recorded almost entirely as an accumulated loss. It amounted to €19.2 billion and was carried forward to the next year. This was the starting point for the financial year 2025.

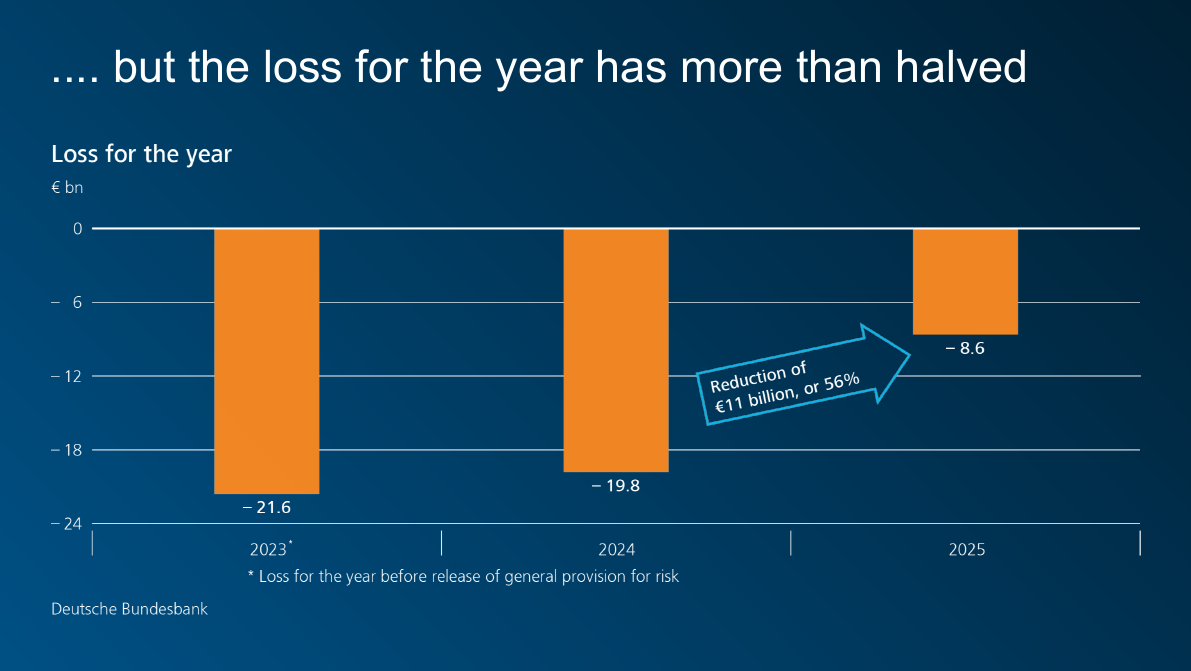

Developments were much as suggested at last year’s annual accounts press conference – although the financial burdens persisted, they were significantly lower than in 2024. There are two main reasons for this: first, key interest rates were lower on average than in the previous year. Second, maturing bonds expired, meaning that interest-bearing deposits also decreased.

The Bundesbank’s loss for 2025 was down by more than one-half on the year. The loss for the financial year 2025 comes to €8.6 billion.

The accumulated loss has risen by this amount and now stands at €27.8 billion. This figure is the sum of the accumulated losses carried forward from 2024 and the loss for the financial year 2025. We will once again carry the accumulated loss over to next year and offset it against future profits.

You can see that the financial burdens are easing from the developments in the annual loss: it fell from €21.6 billion in 2023 to €19.8 billion in 2024 and has now come down to €8.6 billion in 2025.

You can see that, as expected, we are heading in the right direction. The peak annual burdens are behind us. From today’s perspective, this positive development is likely to continue. This is because the monetary policy securities holdings are continuing to decline in line with their maturities. This means that there will also be a decline in deposits on which interest must be paid.

Nevertheless, patience is still required. We still expect net interest income to be negative for the time being. This year, the Bundesbank will report an annual loss again. It will probably be a little smaller than in 2025.

Right now, I am not able to tell you when we will be back in the black. But the Bundesbank’s financial burdens are temporary in nature. Once they are behind us, we can expect surpluses again.

We will use profits from future financial years to reduce the accumulated loss and build up adequate risk provisions, all without external assistance. We therefore do not expect to be able to distribute any profit for a longer period of time.

It is not possible to reliably predict when profit distributions will be possible again. It depends on how key interest rates as well as the size and structure of our balance sheet evolve in the future. This is inherently uncertain.

One thing is clear: monetary policy requirements mean that price stability in the euro area must be safeguarded. That is the Eurosystem’s primary objective. And that is what our actions aim towards. We can and will do everything necessary to achieve this goal.

I am keen to emphasise that even if the Bundesbank reports an accumulated loss, it remains fully able to perform its tasks. As unfortunate as it is to have to report losses, there is one thing we should not lose sight of here: the Bundesbank still has a sound balance sheet.

We have large valuation reserves. They amounted to €388 billion at the end of 2025. They are thus many times larger than the current and prospective accumulated losses. Sabine Mauderer will present you with more detailed information about that in just a moment.

5 Conclusion

Ladies and gentlemen,

On balance, we achieved something very important in 2025: price stability prevails in the euro area once again. Ensuring this on a sustainable basis is our top priority. We will continue to do everything necessary to achieve this aim.

And now I would like to hand over to Sabine Mauderer.

Footnotes:

- Deutsche Bundesbank (2025), What’s behind the sustained decline in German export market shares?, Monthly Report, July 2025.

- Deutsche Bundesbank (2024), Competitive pressure from China on Germany and other advanced economies, supplementary information, Monthly Report, November 2024.

- Deutsche Bundesbank (2025), Forecast for Germany: Economy gradually returns to recovery path, Monthly Report December.

- Weber, M. (1919), Politik als Beruf, lecture held on 28 January 1919 in Munich, in: Weber, M. (1919), Geistige Arbeit als Beruf. Vier Vorträge vor dem Freistudentischen Bund, Duncker & Humblot, Munich and Leipzig, p. 66.

- Bates, C., F. Kuik, E. Wieland and Z. Zekaite (2025), Inside the food basket: what is behind recent food inflation?, ECB, Economic Bulletin, Issue 8; D’Acunto, F., F. De Fiore, D. Sandri and M. Weber (2025), A global survey of household perceptions and expectations, BIS Quarterly Review, September.