How are households’ consumption plans affected by the COVID-19 pandemic? Research Brief | 35th edition – November 2020

This research brief reports how consumption plans and spending propensities were affected at the early stages of the COVID-19 pandemic. An online survey shows that private households have been significantly more cautious in their spending intentions, while the average marginal propensity to spend has remained at an elevated level.

Income developments and income expectations

The COVID-19 pandemic affected the household finances of a substantial percentage of respondents. This is based on the results of the May 2020 wave of the "Bundesbank Online Pilot Survey on Consumer Expectations". The survey solicits individuals’ inflation expectations, expectations with respect to their income, their spending intentions and the effect of the COVID-19 pandemic and the lockdown measures on household income in the early stages of the pandemic.

On average, more than 40% of respondents incurred income or other financial losses due to the pandemic or the policy measures addressing it. The figure is, not surprisingly, higher for those who participate in the labour force (46%) than for those who do not (28%). The latter group comprises mainly pensioners.

Respondents expect their monthly net income to fall, on average, by €64 per month over the following 12 months. Importantly, however, income expectations vary substantially among respondents: 40% expect their income to fall, on average, by more than €500 per month; 8% expect their income to remain the same; 52% expect their income to increase, on average, by about €290. This last group comprises mainly employees and retirees, who expect to retain their job or pension, as well as students who may expect to find a job.

How have spending intentions been affected?

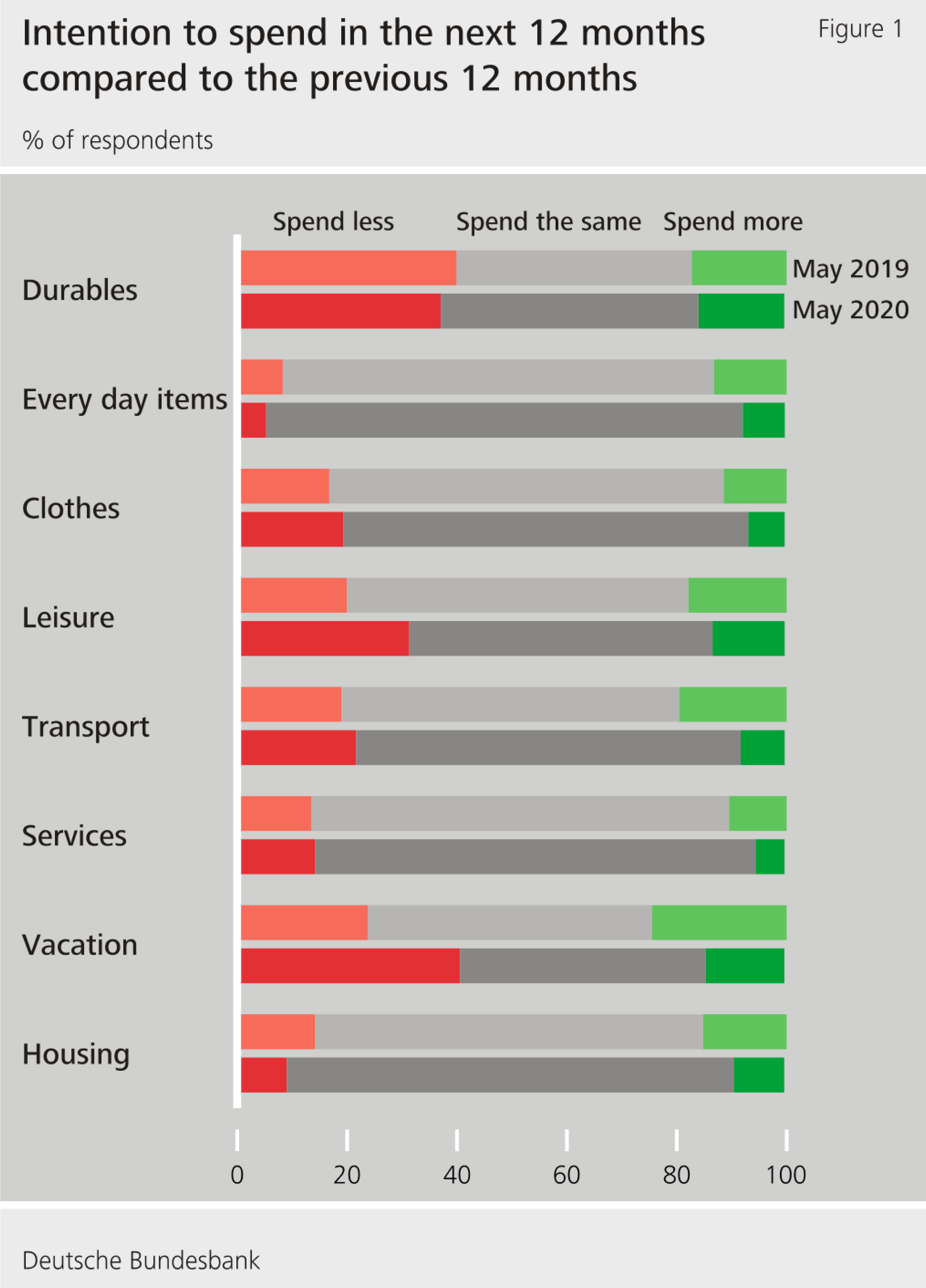

The majority of respondents intend to spend the same over the next 12 months as in the previous 12 months. Yet, compared to May 2019, the percentage of respondents intending to spend more has decreased, whereas the percentage of respondents intending to spend less has increased for several item categories (see Figure 1). Intentions to spend less are driven by coronavirus-induced income losses as well as higher inflation expectations. Respondents with expected income losses are also more likely to intend to spend less on durables and leisure activities. Respondents expecting inflation to be higher intend to spend less on durables. This runs counter to standard economic theory, which suggests that those who expect inflation to be higher should spend more on durables to protect themselves from the increase in inflation (D’Acunto, Hoang, Weber 2020). One possible explanation for this result is that individuals often associate higher inflation with generally unfavourable economic conditions (Bachmann, Berg and Sims 2015, Coibion et al. 2019). Spending intentions may have also been influenced by restrictions in the supply of goods or services, or by other factors related to the COVID-19 pandemic that we were unable to control for.

Propensities to spend in times of COVID-19

We also asked survey respondents how they would spend a windfall payment equal to their monthly household income in the next 12 months. This question captures their marginal propensity to spend. On average, they report that they would spend almost half of this additional income. This is similar to the levels observed in a Bundesbank household wealth survey in 2017 (51%, based on the 2017 Panel on Household Finances), implying that, so far, the average marginal propensity to spend has not changed during the coronavirus crisis.

The marginal propensity to spend has two components: the marginal propensity to consume (MPC) nondurable goods and the marginal propensity to consume durable goods. Respondents report spending, on average, 17% of the windfall gain on nondurables and 32%, on average, on durables, in line with recent work of Christelis et al. (2019) and Jappelli and Pistaferri (2020), who show a high propensity to consume out of one-time payments.

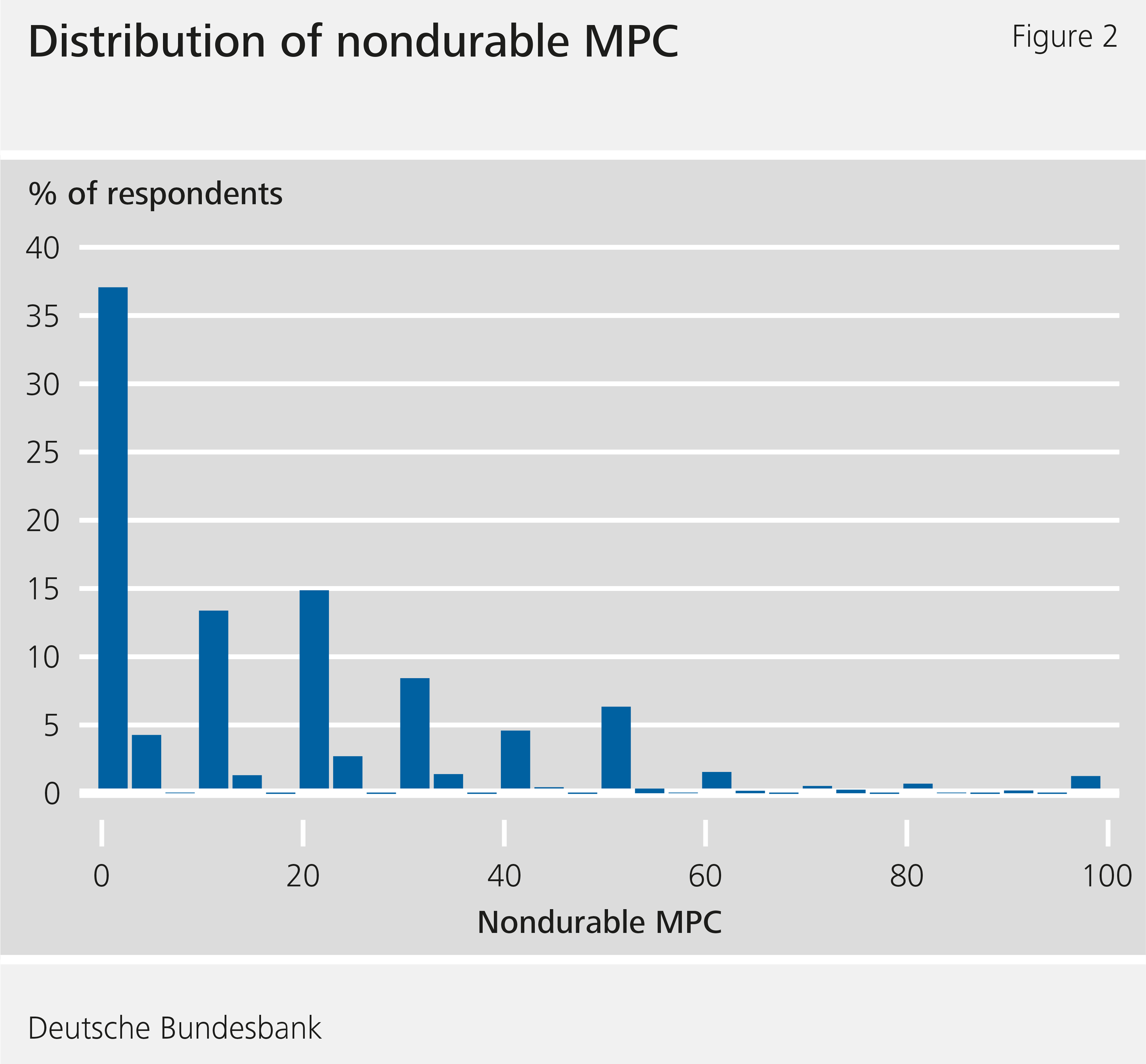

The average MPCs mask considerable heterogeneity among respondents. Figure 2 shows the distribution of the nondurable MPC. About 37% of respondents would spend less than 5% of the windfall. However, around 45% of respondents would spend more than 10%. This heterogeneity is important in determining the overall response of aggregate demand to fiscal or monetary policy stimulus packages (see also Auclert 2019 and Kaplan, Moll and Violante 2018).

What drives the differences in spending propensities?

Inflation expectations and income are key determinants of MPC heterogeneity. A regression analysis reveals that respondents with net income below €1,500 exhibit a 6 percentage points higher propensity to consume nondurable goods compared to respondents with net income above €5,000.

Respondents who expect an average inflation rate between 0% and 2% over the next 12 months report a 5 percentage points higher propensity to consume durable goods than those who expect prices to fall.

Age, home ownership, employment status and income expectations also contribute to heterogeneity in the marginal propensities to consume. But while coronavirus-induced income and financial losses have affected consumption plans, they seem to have only limited effects on marginal propensities to consume, reflecting the fact that liquidity-constrained households often spend large parts of one-time cash windfalls. Even though a hypothetical payment of a one-time stimulus payment resulted in large MPCs, the impact of the announcement of expansionary fiscal and monetary policy measures on subjective expectations is small, as discussed in Goldfyan-Frank, Kocharkov and Weber (2020).

Conclusion

After the relaxation of the pandemic-induced lockdown, a larger percentage of households plans to spend less than before the onset of the pandemic. This effect is more pronounced for households who lost earnings due to the pandemic or who expect future income losses. Thus far, however, the pandemic has had little impact on the average marginal propensity to spend, which has remained at an elevated level. This is encouraging with a view to the effectiveness of the German federal government’s stimulus package. The higher MPC households, being more responsive to the stimulus payments, play a key role in this respect.

Disclaimer |

The views expressed here do not necessarily reflect the opinion of the Deutsche Bundesbank or the Eurosystem. |

Literature

- Auclert, Adrien (2019), "Monetary Policy and the Redistribution Channel." American Economic Review, 109 (6): 2333-67.

- Bachmann, Rüdiger, Tim O. Berg, and Eric R. Sims (2015), "Inflation Expectations and Readiness to Spend: Cross-Sectional Evidence." American Economic Journal: Economic Policy, 7 (1): 1-35.

- Baker, Scott R., Farrokhnia, R. A., Meyer, Steffen, Pagel, Michaela and Constantine Yannelis (2020), "Income, Liquidity, and the Consumption Response to the 2020 Economic Stimulus Payments". NBER Working Paper No. 27097, May.

- Coibion, Olivier, Georgarakos, Dimitris, Gorodnichenko, Yuriy and van Rooij, Maarten (2019), "How Does Consumption Respond to News about Inflation? Field Evidence from a Randomized Control Trial". (July 18, 2019). Available at SSRN: https://ssrn.com/abstract=3426489 or http://dx.doi.org/10.2139/ssrn.3426489

- Christelis Dimitris, Georgarakos, Dimitris, Jappelli, Tullio, Pistaferri, Luigi and van Rooij, Maarten (2019), "Asymmetric Consumption Effects of Transitory Income Shocks". The Economic Journal, 129 (622): 2322–2341.

- D’Acunto, Francesco, Daniel Hoang and Michael Weber (2020), "Managing Households' Expectations with Unconventional Policies". NBER Working Paper No. 27399, June.

- Goldfyan-Frank Olga, Georgi Kocharkov and Michael Weber (2020). "Policy Announcements and Household Expectations - What Could Go Wrong?" Deutsche Bundesbank, Research Brief 34.

- Jappelli Tullio and Luigi Pistaferri (2020), "Reported MPC and Unobserved Heterogeneity". American Economic Journal: Economic Policy (forthcoming).

- Kaplan, Greg, Benjamin Moll, and Giovanni L. Violante (2018), "Monetary Policy According to HANK." American Economic Review, 108 (3): 697-743.

The authors | ||

| René Bernard Research Assistant, Research Centre, Deutsche Bundesbank | Panagiota Tzamourani Senior Economist, Research Centre, Deutsche Bundesbank | Michael Weber Associate Professor of Finance, niversity of Chicago |

News from the Research Centre

Publications

- “Time-varying return correlation, news shocks, and business cycles“ by Norbert Metiu (Deutsche Bundesbank) and Esteban Prieto Fernandez (Deutsche Bundesbank) will be published in the European Economic Review.

- “The Hockey Stick Phillips Curve and the Effective Lower Bound” by Philipp Lieberknecht (Deutsche Bundesbank) and Gregor Boehl (Universität Bonn) will be published in the Journal of Economic Dynamics and Control.

Events

- Spring Conference on Expectations of Households and Firms

24. – 25.04.2025 | Eltville am Rhein